The Dutch carpet industry produced an oil-based product with no economic afterlife. A sector-wide map gave its competitors the shared picture they needed to design a different future, on a horizon stretching to 2030.

Case study7 min read

Most carpets produced in the Netherlands in 2014 were made from polyester and nylon, fibers derived from oil. They performed well in the showroom and the warehouse, and at the end of useful life almost never came back as anything other than landfill or incinerator feedstock. The sector understood the dependency. The trade association MODINT understood it. The question that arrived on Except's desk, brought by MODINT in partnership with DNV, was less whether the dependency could end than how a fragmented commercial sector could agree on the order in which to end it.

An industry locked into its own materials

Dutch carpet manufacturing had inherited a material logic from the second half of the twentieth century, when synthetic fibers were the future and recycling was, at best, a technical curiosity. By 2014, the inheritance had become a liability. Volatile oil prices translated directly into volatile cost structures. Institutional buyers were beginning to ask procurement questions the sector did not have ready answers for. European waste regulation was tightening across textile categories. Adjacent industries, automotive interiors and soft furnishings among them, were already publishing roadmaps of their own.

The structural difficulty was not technical. Bio-based polymer chemistry existed in working pilots. Mechanical and chemical carpet recycling had been demonstrated in laboratory and small-batch settings. What did not exist was a shared picture of how the entire sector, manufacturers, fiber spinners, recyclers, retailers, installers, end-of-life processors, fit together as a single material economy. Without that picture, every individual investment looked premature. With it, the same investments could be sequenced into a chain where one company's waste stream became another's feedstock.

“

A major challenge within the carpet manufacturing sector is securing the right resources to continue production.

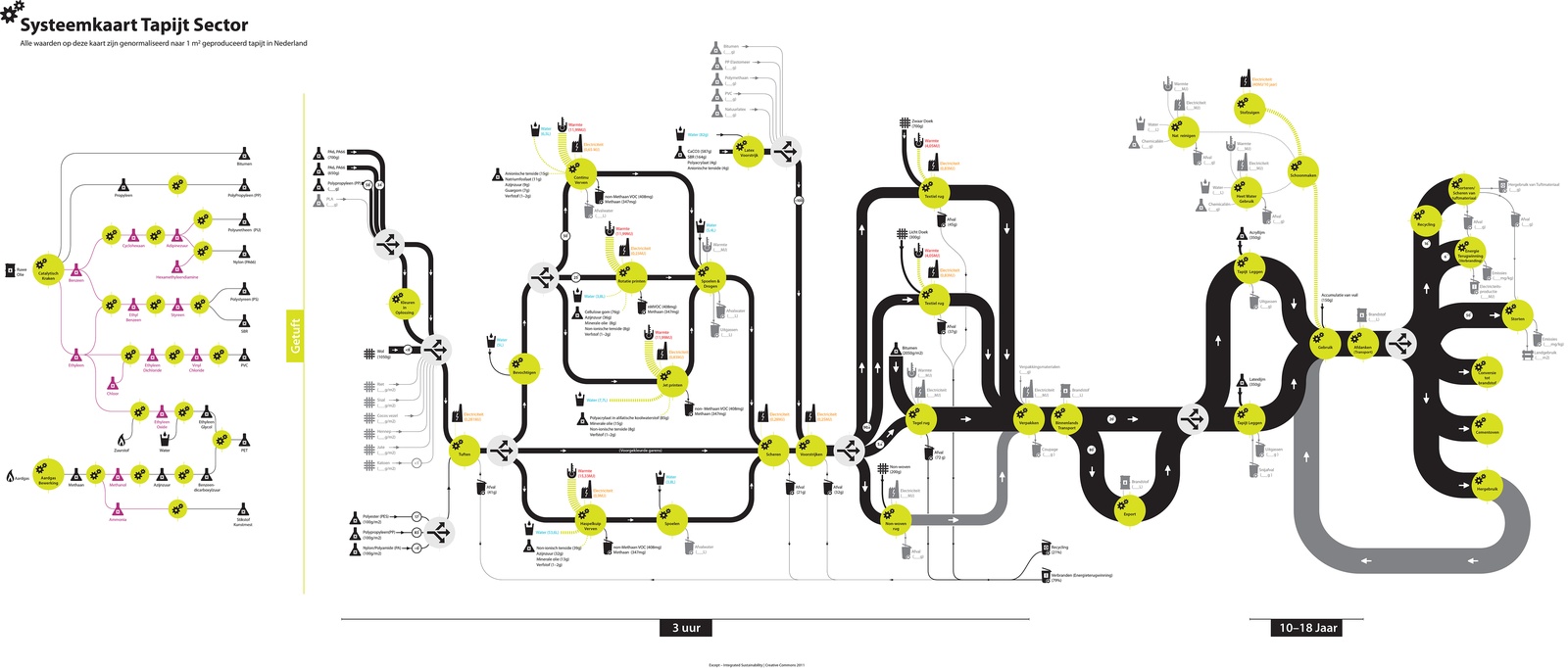

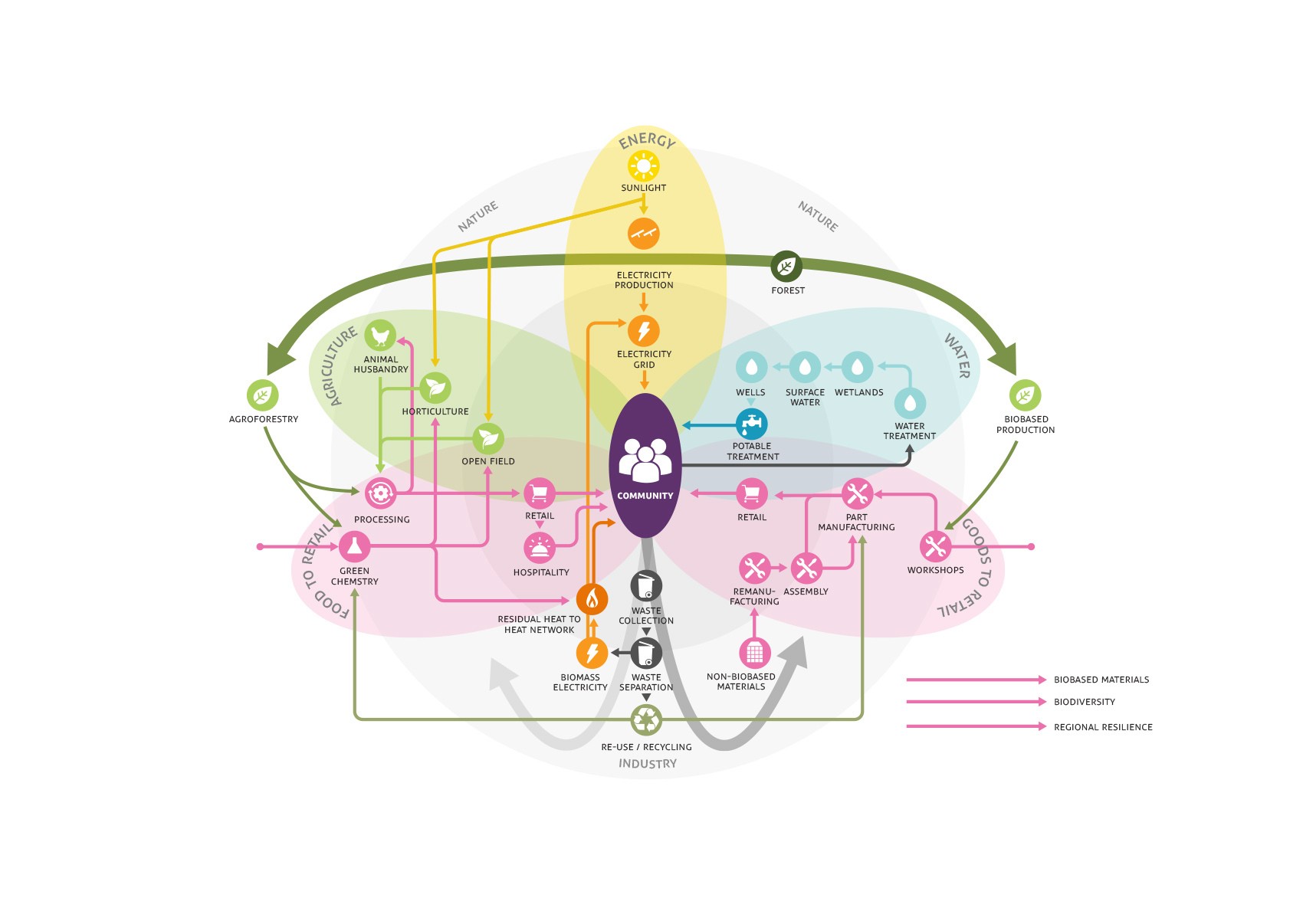

The status-quo map: every significant material flow and stakeholder relationship in the Dutch carpet sector, drawn as a single diagram. The outer ring shows current resource flows. Reading it took as long as building it.

A method built on visualization

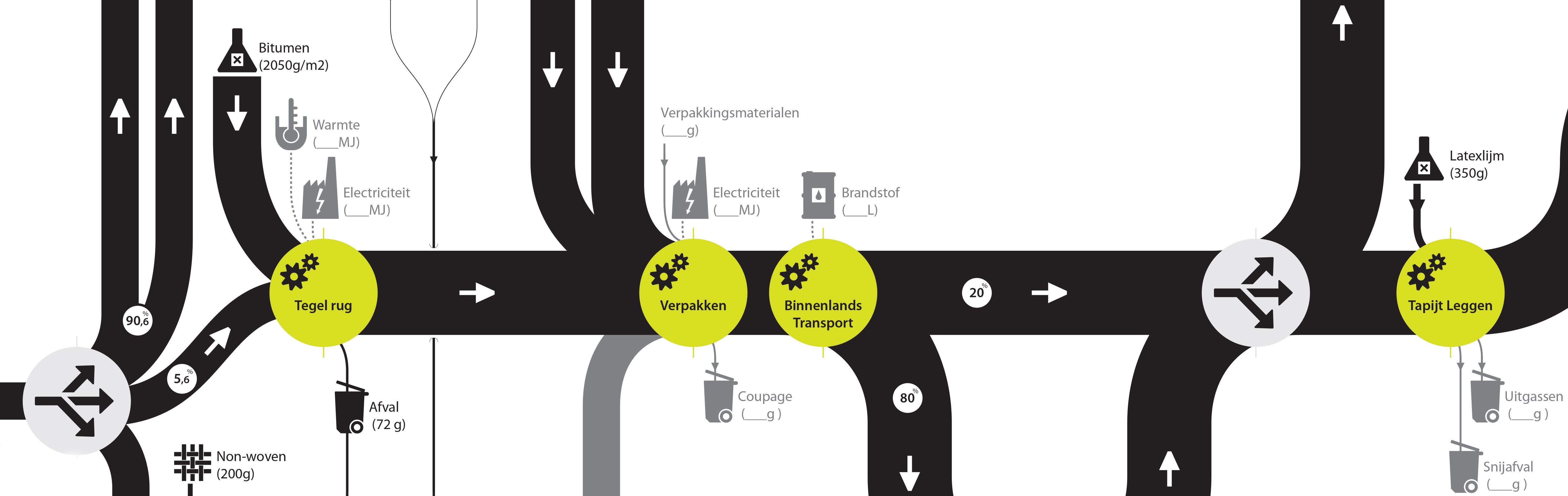

Except's response, working alongside DNV and MODINT, was to produce a map. Not a process diagram or a value-chain illustration, but a full sector-wide visualization that showed every significant material flow and every significant relationship between actors. Two versions were built. The first captured the current state of the industry: oil-based feedstock entering at one edge, finished product exiting at another, dominant flows running in straight lines from supplier to manufacturer to retailer to consumer to disposal.

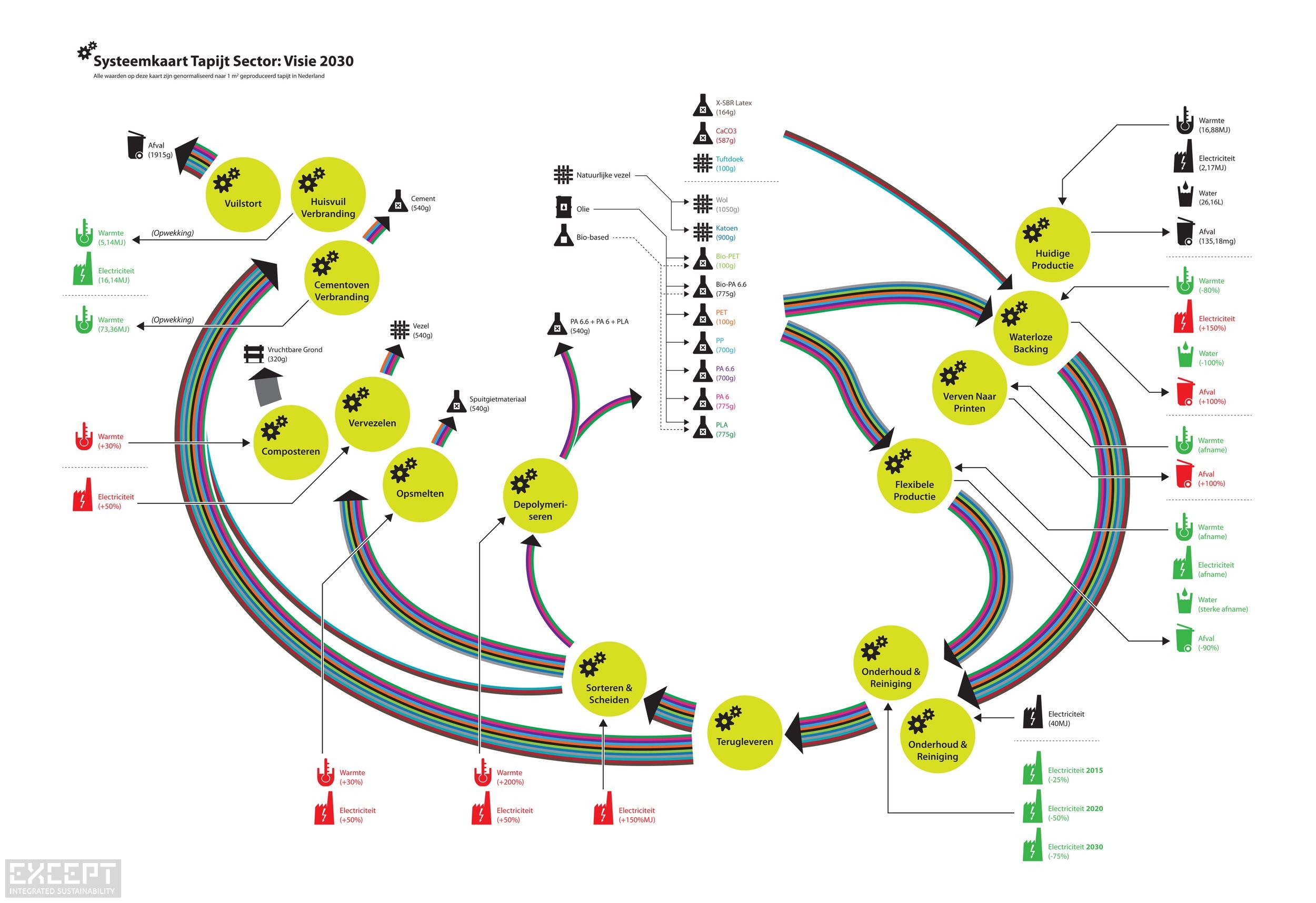

The second version captured a 2030 state. The same actors were arranged differently. New connections were drawn between end-of-life processors and primary producers, between bio-based feedstock providers and existing fiber spinners, between competitors who would share recovery infrastructure rather than build it separately. The two diagrams sat side by side, and the comparison was the argument: here is what the sector currently is, here is what it needs to become, here are the precise points at which intervention is required.

The maps were not graphic-design exercises. They were decision-support instruments. Each connection on the page represented a contractual relationship, a logistical pathway, or a piece of technology that either existed or had to be built. Each gap between the two diagrams identified work that someone, somewhere, would have to take on.

The roadmap, in numbers

2030Target horizon for a fully circular Dutch carpet sector

2Strategic pathways developed: recycling and bio-based feedstock

1Sector-wide map, two states visualized, shared across competitors

600+Projects worldwide using the Symbiosis in Development framework since 1999

Status quo, in detail: linear flows from oil to landfill, with no return pathway visible.

The 2030 vision: new connections, bio-based inputs, shared end-of-life infrastructure where there had been none.

Two bets, neither sufficient alone

The roadmap rested on two non-exclusive strategies. The first was that bio-based materials, polymers derived from plant feedstocks rather than petroleum, could be scaled into commercial fiber production within the available window. The second was that recycling, both of post-industrial waste from the manufacturing process and of post-consumer carpet recovered at the end of its life, could close the loop on the materials already in circulation across European homes and offices.

Neither pathway worked alone. Bio-based feedstocks addressed the entry point of the material flow but did nothing about the volume of synthetic carpet already in service. Recycling addressed the existing stock but depended on a collection and sorting infrastructure that would take years to build, and a market for recovered fiber that did not yet exist at scale. The two bets had to be developed in parallel, with investments timed against each other so that supply and demand for circular materials grew in the same window of years.

The hardest cooperation lives at the intersections: where one company's output has to become another's input.

Governance, not chemistry

The hardest part of the roadmap was not the chemistry or the engineering. It was the governance. Carpet manufacturing in the Netherlands is a competitive industry. Margins are thin. Brand differentiation matters. Companies that compete vigorously for the same accounts cannot easily share information about input costs, supplier relationships, or product formulations, even when sharing would benefit them all.

The system map made it possible to identify a class of cooperation that did not require any single competitor to expose its commercial sensitivities: shared end-of-life infrastructure, joint research on bio-based polymers, common standards for material identification at the point of disposal. These are precompetitive collaborations. They sit upstream of the moment at which firms compete on product, and they create the conditions for that competition to continue without the sector collectively running out of viable inputs.

The mapping process gave the industry a vocabulary for distinguishing precompetitive coordination from anti-competitive coordination, which mattered to general counsel, and it gave chief executives a way to commit to joint work without disadvantaging their own commercial positions, which mattered to boards. Clarity at the system level translated into permission at the company level.

“

Clarity and understanding are vital ingredients for the industry to work together and define programs in which competitors can cooperate and transition toward a circular business model.

The replication question

The Dutch carpet roadmap was one of three sector-level mapping projects Except produced in this period. The wastewater chain followed, again with DNV as partner, on a similar 2030 horizon. The Dutch meat processing industry came after, mapped through the same lens of material flow and stakeholder relationship. The parameters were different in each case. The methodology was the same: build the map, find the precompetitive space, sequence the investments, and treat the diagram itself as the convening document that allows the conversation to happen.

For executives weighing a sector transition, the lesson sits earlier than the technology choice. Before a company can decide what to build, it needs to know what its sector is going to need built. The system map is the artifact that makes that conversation possible across competitors, regulators, and customers who would otherwise talk past one another. Without it, every player optimizes individually and the sector as a whole arrives at its horizon year having made many local improvements and very little structural change.

The Dutch carpet industry now has the map. What it does between here and 2030 is the longer story, written one investment, one supplier agreement, and one shared facility at a time.